the valuation discount hiding in plain sight: an industry survey of M&A risks

in the high-stakes environment of brokerage mergers and acquisitions (m&a), a fundamental truth governs the transaction: buyers do not simply acquire a stream of historical earnings; they acquire confidence in the future of those earnings.

executive summary: the architecture of confidence

in the high-stakes environment of brokerage mergers and acquisitions (m&a), a fundamental truth governs the transaction: buyers do not simply acquire a stream of historical earnings; they acquire confidence in the future of those earnings. when a brokerage’s financial operations rely on manual, spreadsheet-dependent processes, it signals a "confidence discount" to institutional buyers. this discount exists because the business is perceived as harder to verify, more expensive to integrate, and structurally difficult to scale.

this whitepaper serves as a synthesis of industry-leading research from ey-parthenon, forrester, and the institute for mergers, acquisitions and alliances (imaa). it examines how reporting fragility directly erodes enterprise value and why modernization is no longer an operational choice, but a financial imperative.

key takeaway: modernizing finance operations is a primary equity-defense strategy. the transition from fragile, person-dependent processes to a robust enterprise platform is the most direct method to protect a brokerage's valuation multiple and ensure exit readiness.

multiple compression and the confidence discount

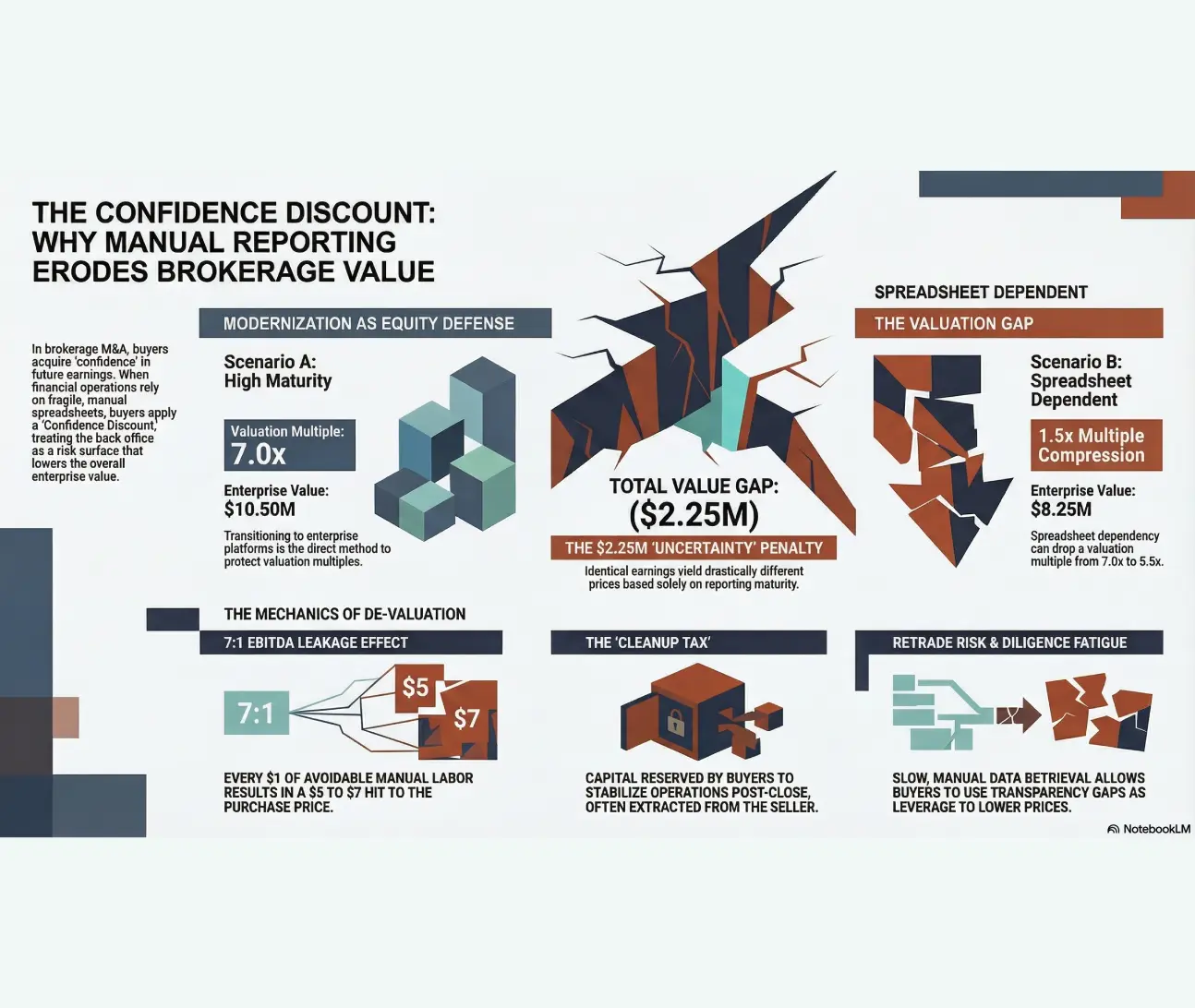

the strength of a valuation multiple is an explicit reflection of reporting maturity. when monthly reporting is delayed, inconsistent across entities, or reliant on complex spreadsheet "bridges," buyers categorize the reported ebitda as "uncertain" rather than "durable." this shift in perception triggers multiple compression, where the buyer applies a lower multiple to hedge against the risk of classification drift, timing errors, or unreconciled balances.

according to forrester consulting, modernized finance operations provide measurable returns in visibility and accuracy. in contrast, the labor-intensive effort required to validate spreadsheet-based results causes buyers to assume the worst, treating the back office as a "risk surface."

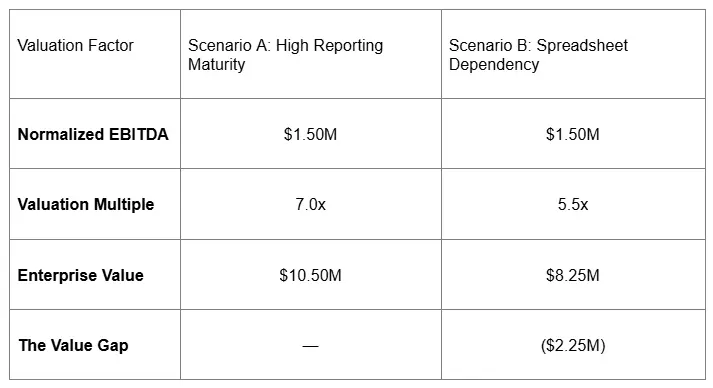

the value gap: reporting maturity vs. spreadsheet dependency

the table below quantifies the "confidence discount." while the underlying earnings are identical, the maturity of the reporting system dictates the final purchase price.

market context: in the current climate, smaller or more transactional brokerages typically see multiples in the 4x–6x range with strong reporting maturity. without it, valuations are further compressed through the mechanisms of uncertainty and perceived risk.

the “cleanup tax” and EBITDA leakage

beyond the headline multiple, operational gaps create explicit financial deductions and structural protections that favor the buyer.

EBITDA leakage: the multiplier effect

spreadsheet-dependent operations suffer from "ebitda leakage"—the persistent administrative drag of manual labor, duplicate entries, and exception chasing. from an m&a perspective, this leakage is catastrophic. because valuation is a multiple of margin, every 1 of avoidable manual labor or rework results in a 5 to $7 hit to the final purchase price. in a sale, operational inefficiency is not just a cost; it is a de-valuation.

the cleanup tax and structural protections

the "cleanup tax" represents the capital a buyer must reserve to stabilize finance operations post-close. to mitigate the risks of unorganized charts of accounts or a lack of intercompany discipline, buyers utilize four primary structural protections:

- direct purchase price reduction: lowering the top-line offer to account for known risks.

- escrows and holdbacks: withholding a portion of the proceeds to cover remediation costs.

- shifting value into earnouts: moving guaranteed payments into performance-based milestones to shift integration risk back to the seller.

- mandatory pre-close remediation: requiring the seller to fix operational gaps as a condition of the deal.

vignette: the reality of forensic restructuring consider the common scenario of a multi-entity brokerage utilizing quickbooks paired with excel-based commission tracking. this setup invariably fails to produce the transparency required for institutional diligence. in such cases, the remediation isn't a mere "cleanup"—it is a forensic restructuring of financial statements to make them trustworthy for third parties. this is a zero-sum game: someone must pay to make the numbers diligence-ready. if the seller has not invested in reporting maturity pre-close, the buyer will extract that cost from the purchase price.

diligence fatigue and retrade risk

fragile reporting processes inevitably lead to "diligence fatigue." when a seller relies on key individuals to perform "forensic spreadsheet archaeology" to answer every data request, the deal cycle slows. this delay increases "retrade risk," where the buyer uses emerging surprises or a lack of transparency as leverage to lower the price or walk away entirely.

checklist: requests that expose spreadsheet dependency

buyers use targeted requests to test the robustness of the finance department. if these cannot be produced quickly and consistently, spreadsheet dependency is exposed:

[ ] trailing 24 months (t24): monthly reporting both consolidated and by legal entity.

[ ] intercompany schedules: detailed elimination logic for cash and expense flows.

[ ] reconciliations: monthly proof for cash, a/r, a/p, commissions payable/accruals, and suspense/clearing accounts.

[ ] ebitda bridge: a clear path from net income to normalized ebitda with consistent, defensible rules.

[ ] audit trail discipline: evidence for significant adjustments and reclassifications.

[ ] policy clarity: clear definitions of cost of sales (cos) vs. opex with absolute consistency across all entities.

guidance from the imaa emphasizes that these it and process gaps create "hidden costs" that directly diminish transaction value and increase the probability of deal failure.

the multi-entity complexity multiplier

real estate brokerages are uniquely susceptible to valuation discounts due to their structural complexity. multi-entity environments amplify operational risks because they involve non-linear compounding of data:

- complex inter-company cash and expense flows.

- high transaction volumes that break manual systems.

- varied and complex commission plan requirements across different regions or teams.

- the necessity for clean multi-entity consolidation and intercompany discipline.

ey-parthenon research indicates that technology and operating-model changes are the primary drivers of integration burdens. for a multi-entity brokerage, a "mess" at the entity level compounds exponentially during consolidation. if a buyer views the back office as a collection of fragmented manual processes rather than an integrated enterprise platform, they will price in a massive integration-cost buffer.

conclusion: modernization as equity-defense

in an unforgiving m&a market, the ability to produce "repeatable financial truth" is a strategic necessity. buyers are no longer satisfied with "pretty financials" provided in a static pdf; they require a close process that produces consistent numbers, supported by a clear audit trail, without manual workarounds.

transitioning from fragmented spreadsheets to a centralized enterprise platform is not a back-office expense. it is a calculated investment in protecting a brokerage's most valuable asset: its equity. by eliminating reporting fragility, owners reduce perceived integration costs, minimize retrade risk, and maximize their ultimate exit value.

selected bibliography

armanino: "family limited partnership solves complex real estate reporting..." (2022).

ey-parthenon: "beyond the deal: accurately estimating m&a integration costs" (2024).

forrester consulting: "the total economic impact™ of sage intacct" (2024).

institute for mergers, acquisitions and alliances (imaa): "m&a’s hidden costs: it due diligence and avoiding post-deal surprises" (march 26, 2025).

about AccountTECH

for over 25 years, AccountTECH's team of real estate accountants and software engineers have been building tools that increase the efficiency of brokerages. their latest flagship product is darwin.Cloud – a 4th generation evolution of their popular real estate accounting software. the team is constantly adding automation and integrations towards the goal of a single point of entry. their motto is: data entry can happen anywhere, but everything winds up in darwin. in their work with clients, partners, and each other, they bring integrity to every interaction and every line of code.

for sales inquiries, please contact:

Theresa Hurt

theresa@accounttech.com

(978) 710-0071

ready to evolve?

request a demo or learn more about the power of darwin.Cloud